3 – The Upcoming Freedom To Surcharge Customers Will Be Closely Monitored By Ottawa

Since Visa and MasterCard largely increased credit card transaction fees in 2008, retailers across the board have been urging Ottawa to limit these abusive costs by imposing a regulatory rate cap, as in Europe.

Since Visa and MasterCard largely increased credit card transaction fees in 2008, retailers across the board have been urging Ottawa to limit these abusive costs by imposing a regulatory rate cap, as in Europe.

However, 10 years later, Ottawa still rejects this solution, preferring cosmetic reductions through voluntary agreements. Why?

In a series of articles entitled “The Secret Memos of Bill Morneau”, DepQuébec tries to understand the Federal government point of view on this issue after having obtained for the first time highly secret and sensitive ministerial memos through the access to information Act.

Today, for the series third part, DepQuébec is looking into the upcoming removal of the no-surcharge rule which will allow Canadian retailers for the first time to charge credit card fees of their own.

Such news could not have come at a better time.

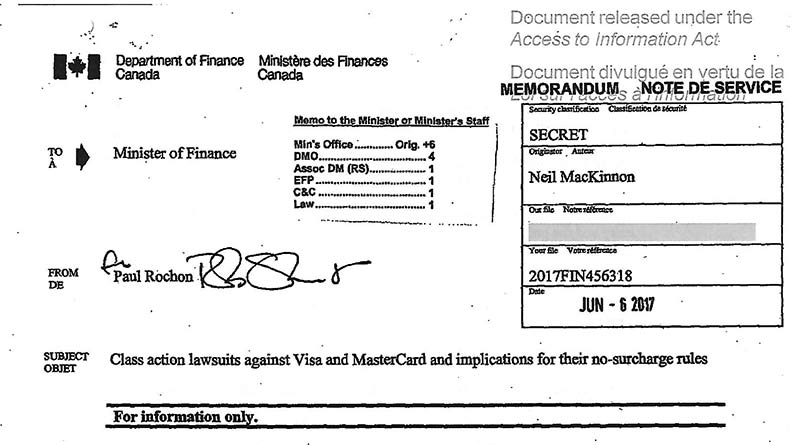

Just after Finance Canada had finished consulting about 20 groups (see Part 2 of this series) and began to think about what to do next, a secret memo dated June 6, 2017 informed Finance Minister Bill Morneau of a major breakthrough.

In the wake of class action lawsuits against Visa and MasterCard filed in Canada’s five most populous provinces, both companies were about to announce settlement agreements allowing retailers to surcharge customers paying with credit cards, similar as changes made to their network rules in the United States since January 27, 2013.

In other words, Visa and MasterCard are finally calling the end of the unfamous No-Surcharge rule in Canada!

A true revolution for Canadian retailers and above all, the long awaited end of an unfair rule prohibiting them to recoup significant costs.

An insightful memo

Labelled “For Information Only”, the memo prepared by Deputy Minister Paul Rochon informed the Minister of the ongoing development before it was made public.

“Settlement agreements regarding class action lawsuits against Visa and MasterCard may be imminent. This note explains potential implications for the no-surcharge and honour-all-cards rules of these two networks.” — Paul Rochon, Finance Canada, June 6, 2017

Recalling that agreements have already been reached with some banks involving substantial dollar amounts of compensation (including Desjardins for $ 9.9 million), the memo explains that Visa and MasterCard settlement agreements will lead to much deeper changes by finally allowing merchants to surcharge customers using credit cards.

Soon, Canadian retailers will be allowed to charge additional fees — if they want to — to customers paying by credit card, under the following conditions:

- The merchant can surcharge at the brand (i.e. networks such as Visa or MasterCard) or product level (e.g., for premium cards), but not both;

- The merchant must notify its acquirer (i.e. Moneris and the likes) of their intent to surcharge at least 30 days prior to implementing surcharging;

- The merchant must provide disclosure of the surcharges to customers at the point of entry and the point of sale;

- The surcharge amount must be identified separately on the transaction receipt;

- If the merchant accepts a competing network brand, it may surcharge only in the same way it would surcharge the competing network;

- If the competing network prohibits the merchant from surcharging, the merchant may not surcharge unless it also surcharges the competing brand’s cards.

A week later, as a matter of fact, Visa and MasterCard unveiled the agreements in separate press releases (see here and here). The precise modified rules agreed for each network can be accessed here (Visa) and here (MasterCard).

To the heart of the matter

As the very existence of this memo indicates, the significance of this outcome didn’t go unnoticed.

“The potential impacts of the settlement agreements on credit card fees were considered as part of the credit card fee assessment announced by the Minister of Finance on September 14, 2016”, confirmed Finance Canada in an email to DepQuebec.

Indeed, one couldn’t overestimate the importance of the No-Surcharge rule in disputes between retailers and credit card companies.

This notion is at the very heart of the issue as well as a key factor behind the controversial rates that the industry would like to see capped.

In this regard, the Competition Tribunal’s decision is most enlightening.

In its lawsuit against Visa and MasterCard, the Competition Bureau argued that surcharging is effective at steering transactions to lower cost methods of payment and that the ability of merchants to surcharge or threaten to surcharge on credit cards constrains the level of Card Acceptance Fees.

One of the expert witnesses from the Competition Bureau, Ralph Winter, professor of economics at UBC Sauder Business School in British Columbia, came to explain this rationale.

“A retailer can’t switch customers from credit card to cash. That means the merchant response, when, say, its merchant fees go up on credit cards, is not as strong as it would otherwise be in his ability to substitute away from high-cost credit cards.” — Ralph Winter, PhD

Another witness, IKEA’s Charles Symons, subsequently explained that from 2004 to 2010, the IKEA Group applied an additional 70 pence (approximately $1.10) to all UK credit card transactions in its retail stores.

Thus, in 2005, the volume of credit card transactions in these stores decreased by 37% and the number of debit card transactions increased by 16%.

The expected impact of a major transformation

In the United States, the No-Surcharge rule was modified in 2013 and, according to this article, is now mainly used by independent retailers, with some charging fees of up to 3.5%.

Large chains, it seems, refrain from demanding such fees. At Circle K, a well-known c-store banner owned and operated by Alimentation Couche-Tard in the United States, there is no surcharge on credit card payment (we called a few stores to verify). There is even a Circle K Visa credit card with redeemable points at Circle K, which is certainly indicative of a less tense relationship south of the border between the c-store giant and credit card companies.

In addition, a dozen states have passed legislations since 2013 prohibiting surcharges on credit cards. These laws are however being withdrawn one by one following decisions of superior courts deeming them unconstitutional on the basis that they restrict how the price is communicated (source: here).

In Australia, surcharges have been allowed since 2003. However, according to an Australian study cited by the Competition Bureau, 30% of merchants have imposed additional fees on at least one of the credit cards that they accepted in December 2010 against just over 8% in June 2007 (source: here).

This means that surcharges can take some time to get widely adopted, most likely because no one wants to be seen as the first to impose these fees at the risk of seeing the customer depart.

Visa argued that it would not necessarily fear a loss in its transaction volume due to surcharging if cardholders could simply patronize non-surcharging merchants. But this would be the case only if surcharging does not become widespread.

A relief expected by many

However, in Canada, a major and immediate impact is expected for many types of merchants:

- those who do not currently accept credit cards because fees are too expensive will now be able to offer them with fees;

- those who feel they are paying so much as to put their business at risk will now be able to reduce their costs significantly by pocketing fees and lowering the volume of credit card transactions;

- those who do not have a direct competitor nearby (across the street or next to it) may dare to surcharge without risking seeing the customer go elsewhere.

Those who offer gasoline, on the other hand, may be more hesitant to surcharge knowing that the vast majority of customers prefer to pay gas by credit card.

That being said, this modified rule remains a major win for retailers as they now gain unparalleled control over these costs.

It re-establishes de facto much of the balance and power in favor of retailers, because the fact of not being able to rebill such expenses is a flagrant abuse and recognized as such by the Competition Tribunal, hence the settlement agreements announced by Visa and MasterCard.

And as for the proposed regulatory cap on rates, this development has most probably influence Ottawa to wait and see the consequences of such a change in the business model.

“The Department of Finance will monitor the impacts of any changes to the no-surcharge rules. It will be up to individual merchants to determine how best to operate under the revised network rules”, declared Finance Canada to DepQuebec.

In Part 4 of our series, we will examine the Federal government’s strategy adopted towards credit card companies in the wake of these changes.