1 – Volontary Agreement Or Regulatory Cap? Bill Morneau Merely Followed Senior Aides’ Advices

Since Visa and MasterCard largely increased credit card transaction fees in 2008, retailers across the board have been urging Ottawa to limit these abusive costs by imposing a regulatory rate cap, as in Europe.

Since Visa and MasterCard largely increased credit card transaction fees in 2008, retailers across the board have been urging Ottawa to limit these abusive costs by imposing a regulatory rate cap, as in Europe.

However, 10 years later, Ottawa still rejects this solution, preferring cosmetic reductions through voluntary agreements. Why?

In a series of articles entitled “The Secret Memos of Bill Morneau”, DepQuébec tries to understand the Federal government point of view on this issue after having obtained for the first time highly secret and sensitive ministerial memos through the access to information Act.

Today, for the series first part, we look at the issue in general and the historical period covered by the secret memos.

It was on a beautiful Thursday morning, August 9, that the curtain fell in a nice grocery store in Ottawa.

Finance Minister Bill Morneau put an end to retailers’ wildest hopes by announcing a second five-year voluntary agreement between the Federal government and Visa | MasterCard.

Under this voluntary undertaking as they call it, credit card transaction fees will decrease by only 6.7% for the 2020 to 2025 period, down only to 1.40% from 1.50%.

However, while not insignificant and always welcome, these disapointing savings represent indeed crumbs in the eyes of retailers.

The industry was expecting better, much better, given that Canada is the country featuring the highest credit card rates in the world.

Something like a regulatory ceiling limiting the average fee paid by merchants to 0.5% on all cards, at the most!

Which is precisely what the private Member’s bill C-236, tabled by Liberal MP Linda Lapointe on February 2016, had suggested and created expectations for, and which the government seemed to support … until this fateful morning.

So what happened between the tabling of Linda Lapointe’s bill in February 2016 and the announcement of August 2018, which resulted in the government turning its back on a regulatory cap?

Why did Ottawa abandon this option that would have eliminated billions of dollars in artificial costs from consumers’ groceries and from thousands of retailers?

Or to put it simply: what the heck is the Federal government afraid of?

Secrets memos obtained for the first time

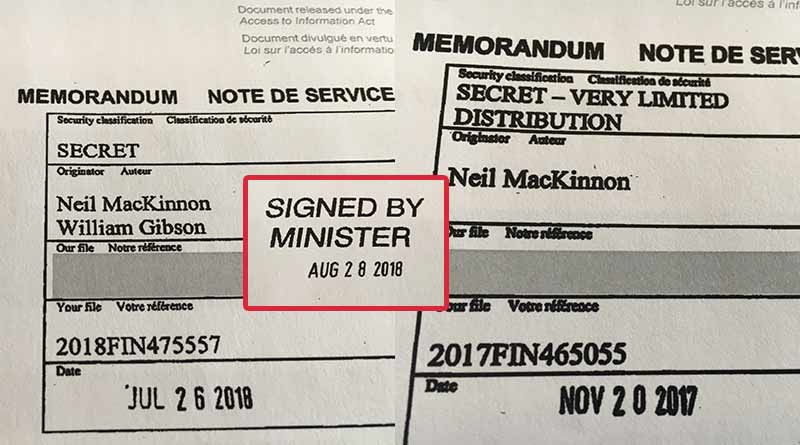

Because these are crucial issues for the future of the retail industry and a major source of frustration for most retailers, many of whom – especially those who sell gasoline – are forced to pay the equivalent of their annual gross benefits in credit card fees, DepQuébec requested and was granted an exclusive access to no less than 10 highly strategic memoranda prepared for the Minister of Finance, Mr. Bill Morneau, for his information and approval specifically concerning the credit card fees issue.

Highly redacted and all written in the English language, these ultra-secret internal memos unveiled for the first time contain precious clues as to why the government shied away from a regulatory ceiling that would have solved the issue once for all.

The sensitivity of the information contained in these memos is undoubted as evidenced by their classification “SECRET” or “SECRET – VERY LIMITED DISTRIBUTION” of which they are labelled.

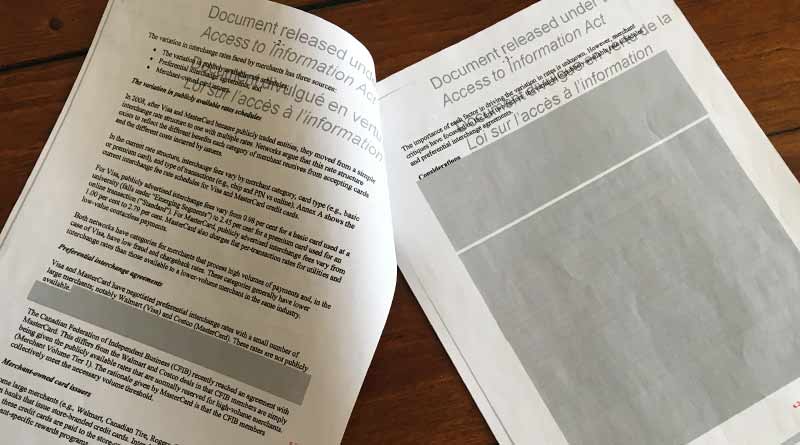

A global context favoring retailers’ demands

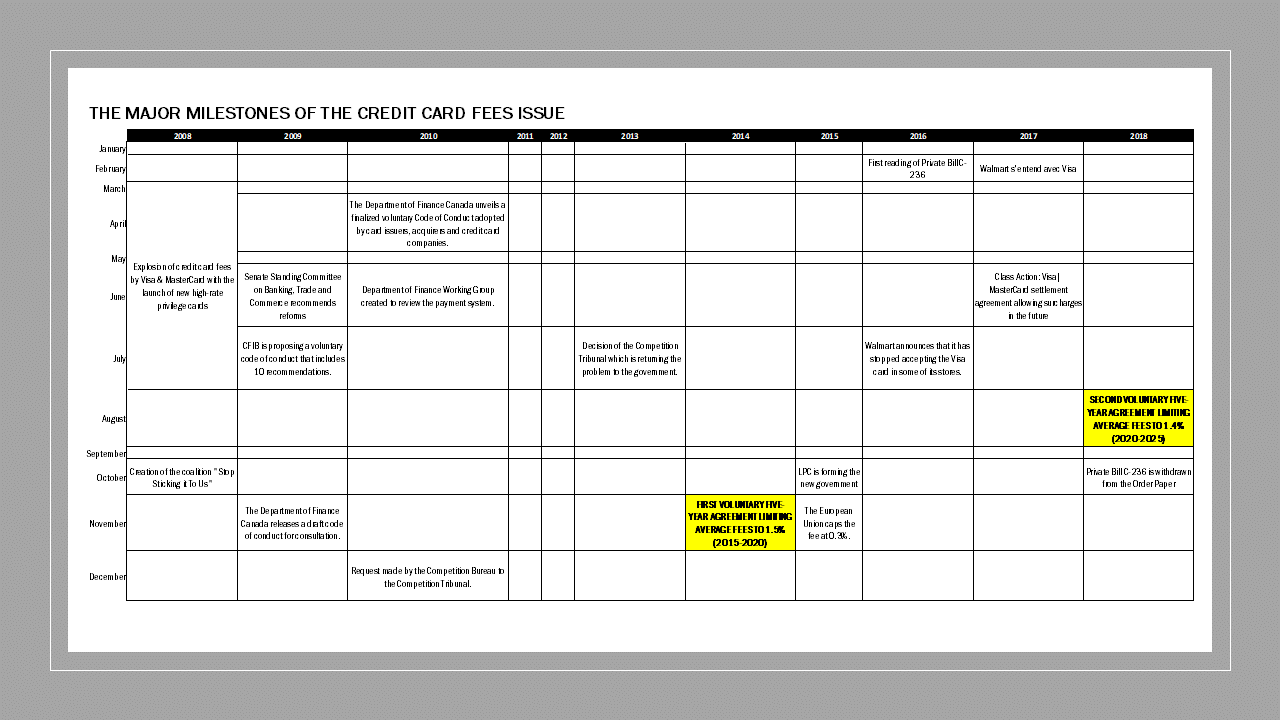

The history and background of the credit card transaction fees issue in Canada is relatively complex but can be summarized simply by isolating a few important important dates and breakthrough, as folllows:

Faced with the unbridled increase in credit card fees caused by the launch and marketing of new high-rate and increasingly used privilege cards, the retail industry trapped by these costs has managed year after year to make some significant gains:

- In 2010, a voluntary Code of Conduct, proposed by CFIB and subsequently adopted by Ottawa, brings more transparency and clarity to the business practices of issuers, acquirers and credit card companies;

- In the same year, the Competition Bureau takes side for retailers and initiates a lawsuit against credit card companies to the Competition Tribunal;

- In 2013, the Tribunal partially rules in favor of the Competition Bureau but leaves any future action to the government;

- In 2014, the Conservative government announces a five-year voluntary agreement that reduces credit card fees by about 10%, to an average rate of 1.5%;

- In 2016, Linda Lapointe tables private Member’s bill C-236 which would give the Minister of Finance the power to cap rates by regulation;

- In 2017, Visa and MasterCard agree to remove their No-Surcharge policy in certain provinces (including Quebec) in the near future, in response to a class action brought against them;

- In 2018, Ottawa announces a second voluntary agreement limiting rates to 1.40%, from 2020 to 2025.

However, none of these gains (except maybe the no-surcharge rule removal which we will discuss later on) are significantly removing the burden of these fees on retailers so that they will likely remain quite high in Canada for at least another 6 years, until 2025 unless, of course, there is a change of government and a 180-degree turn on this policy, which seems very unlikely and uncertain.

In this series second part, we will look at how the federal government sees the role and place of credit cards transactions in the national payment system and how it fits into the country’s strategic economic interests.