5 – Not delivered on Year 1, it’s Been Radio Silence Since Then on the Promised 1.50% Reduced Rate

Since Visa and MasterCard largely increased credit card transaction fees in 2008, retailers across the board have been urging Ottawa to limit these abusive costs by imposing a regulatory rate cap, as in Europe.

Since Visa and MasterCard largely increased credit card transaction fees in 2008, retailers across the board have been urging Ottawa to limit these abusive costs by imposing a regulatory rate cap, as in Europe.

However, 10 years later, Ottawa still rejects this solution, preferring cosmetic reductions through voluntary agreements. Why?

In a series of articles entitled “The Secret Memos of Bill Morneau”, DepQuébec tries to understand the Federal government point of view on this issue after having obtained for the first time highly secret and sensitive ministerial memos through the access to information Act.

Today, for the series fifth part, DepQuebec is examining the third-party verification process of Visa and MasterCard voluntary interchange rate reductions.

In the previous parts of this series, we examined how and why the Federal government preferred to enter twice into temporary voluntary agreements with Visa | MasterCard rather than imposing a regulatory cap on interchange rates.

Such decision is not without some merit but one has to make sure credit card companies live up to their commitments.

Hence Ottawa’s important precaution of requiring “annual third-party verifications” to ensure that these are met.

However, in a rather disturbing way, there are two things that we now know for sure about the first five-year voluntary undertakings that began in April 2015 and which opened the door to a second one announced last summer:

- 1) at the end of Year 1, we have proof that both Visa and MasterCard have failed to reduce their average interchange rate to 1.50%, as promised;

- 2) the government won’t give out any detail for Year 2 and 3, insisting that third-party reports are strictly confidential.

The problem here is that we must rely solely on Ottawa’s reassurance.

Unfortunately, as for Year 1, it has proven to be misleading.

Which leads us to question this whole third-party verification process that is being done under a shroud of secrecy!

If this is not distorting the truth, than what is it?

In September 2016, it hasn’t been a year yet since Finance Minister Bill Morneau got in office.

During that month, he released his first public declaration ever on the credit card fees issue, some seven months after Bill C-236 was tabled by his colleague MP Linda Lapointe who took on her to champion the issue.

« The Government of Canada acknowledges the independent audit findings that both Visa and MasterCard have met their respective commitments to reduce credit card interchange fees,” — Department of Finance, Sept. 14 2016 press release

It was a clear statement. The commitments have been fulfilled. And what exactly are they? If we refer to the Department of Finance initial release issued in 2014, they were as follows:

In other words, “meeting their respective commitments” can’t mean anything else than having succeeded at reducing credit card fees to an average of 1.50% for that first year.

Because the commitments are not just about reducing rates, but doing so as to reach an average ceiling of 1.50% for each one of the agreement’s five years.

However, it has not been the case.

This target has not been reached, neither by Visa which missed it by quite much (starting from 1.61% of average), nor by MasterCard (starting from 1.74%).

Thus, instead of having lowered its average rate by 11 basis points in 2015-2016 as it had committed to do, Visa only dropped it by 8 basis points, a significant difference of 27, 3%.

So why did the Federal government say that they have met their commitments when they haven’t in reality?

Secret memos are telling the truth

In the August 15, 2016 secret memo, we can read the following:

“The Visa report indicates that Visa has reduced its average effective interchange rate to 1.52 per cent and we understand from discussion with MasterCard officials that they have also reduced their average effective interchange rate to a similar level. As stated in their respective agreements, both Visa and MasterCard have laid out plans to further reduce their interchange fees to the 1.50 per cent for the next 12-month period.” — Paul Rochon, Finance Canada Deputy Minister

Two basis points above the target may not look like much, but it’s huge. These represent millions of dollars of overcharged fees to retailers.

For example, the second voluntary agreement announced recently aims at lowering rates by another 10 basis points, saving $250 million over five years for SMEs.

It basically means that every basis point of reduction represents $5 million a year in savings for businesses.

So we are talking here of potentially $10 million in fees that Visa and MasterCard would have overcharged to SMEs in Year 1, based on Finance Canada’s own estimates.

Why such an easy ride?

Ottawa’s attitude is troubling because it seems to be siding closely with credit card companies that have not fully met their commitments.

Even worse, it remained silent upon receiving the annual audit reports for Year 2 (2016-17) and Year 3 (2017-18), as if these important verifications no longer mattered.

Questioned by DepQuebec about the existence and content of these two missing reports, its reponse was the following:

Unfortunately, both Visa and MasterCard failed to answer our requests.

But the fact that Finance Canada puts Year 1 on the same footing as Year 2 and 3 conveys the impression that rates could well be 1.52% or even higher for each of those years and there would be nothing wrong!

They don’t seem to care at all.

Trust us… with eyes closed

The more we delve into this third-party verification process, the more doubts we have.

For example, in the secret memo dated August 15, 2016, one can read the following:

Good to see some admission of guilt. But did these plans work? Nobody knows.

Then, having reached 1.52% in year 1 instead of 1.50%, why not requiring that they reach 1.48% in Year 2 to compensate? Why didn’t Ottawa demand it?

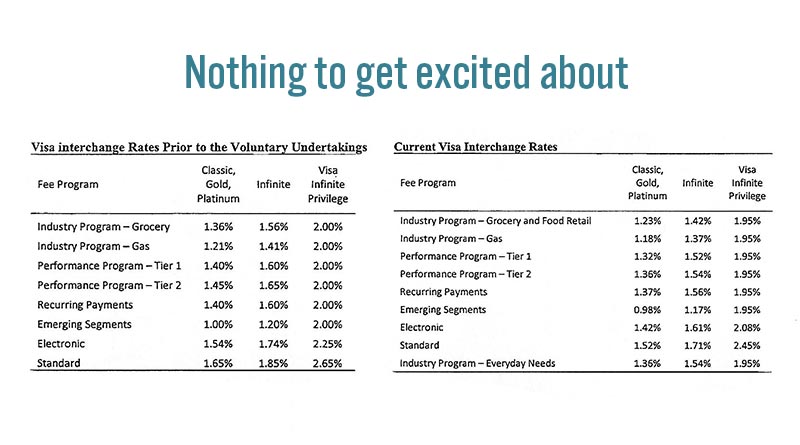

Finally, how on earth could Visa and MasterCard have lowered their average rate by 10% in 2015-2016 (according to Finance) when we know that most of their effective rates fell by just 2.5%? (see source HERE).

Thus, in the grocery category, the rates for a conventional card went from 1.36% to 1.33% (-2.22%), for an Infinite card from 1.56% to 1.52% (-2.56%) and for a privilege card, from 2.00% to 1.95% (-2.50%). We are far from 10%!

Also, by which type of formula is it possible to reach their targets knowing that the proportion of card use, currently experiencing a steady growth, varies from year to year?

And is this average measured by industry? Province? Sector? Type of business? And according to the volumes of each?

We have NO idea which methodology these results are based on, whose lack of accuracy could translate into millions of dollars in overcharged fees to retailers.

Knowing which scientific research approach is used, one could then ask some specialist or academic to validate it.

As is it, our only option, guess what, is to trust the government.

Ottawa’s credibility in doubt

Ottawa’s lack of assertiveness in making credit card companies accountable is supported by three undeniable facts:

- blindly endorsing the first annual report when it was clearly known that Visa | MasterCard failed to reach their 1.50% target;

- demanding nothing in return despite having missed the 1.50% target in the first year;

- not following up on subsequent audit reports (those of Year 2 and 3) like if they don’t matter at all.

This attitude gives the impression that Ottawa fears the power of the credit card giants.

It leads us to believe that retailers are being let down once again, the devil being, as always, in the details.